Of all the things that might one day be regarded as the high-point of pandemic-era financial overexuberance, the $69 million sale of a digital artwork – Everydays: The First 5000 Days – has a solid claim to the top spot.

In March 2021, with much of the world under coronavirus restrictions, the auction quickly made headlines. But while ‘Beeple’ – an American called Michael Winkelmann, whose works had sold for $100 just six months earlier – enjoyed a brief spell of fame, it was the medium itself that was getting investors worked up.

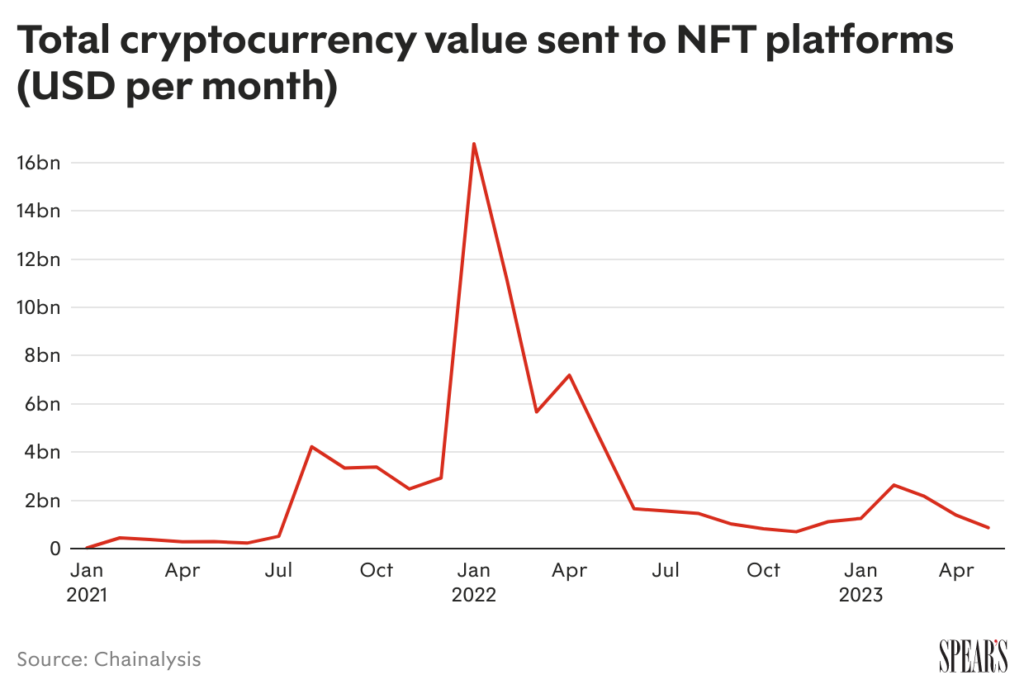

Within weeks, sales of NFTs (non-fungible tokens) had risen by more than 20,000 per cent. By the summer of 2021, the world was spending about $10 billion per month on them, with some collections – notably the pixelated characters known as Crypto-Punks and Bored Apes – regularly changing hands for seven figures.

The excitement wasn’t just financial. As their values soared, NFTs were touted as integral to the next iteration of the internet: the metaverse. Consultants at McKinsey predicted this brave new world would create $5 trillion in value by 2030, while tech investor Andreessen Horowitz launched a new $4.5 billion fund backing all things web 3.0 – including NFTs.

Related

The tide turns on NFTs

The parallels with the dizzying rise of Bitcoin were too tempting for many investors to resist. One survey suggested that as many as four million Americans bought into the NFT craze during its peak. Yet within 18 months, the tide had gone out – almost entirely. According to blockchain adviser Chainalysis, spending on NFTs plummeted by 87 per cent over the course of 2022.

‘Looking back, I think that a lot of the rush was driven by the “greater fool” principle,’ says David Abner, an ETF (exchange-traded fund) specialist and founder of advisory firm Dabner Capital Partners, who was working for the crypto exchange Gemini (founded by the Winklevoss twins) at the time. ‘People were buying them on the expectation someone else would pay more in a week’s time.’

Winners and losers

Of course, not everyone was wrong in that hypothesis. For a small clique of early adopters, the returns were eye-watering. According to cryptocurrency analyst Nansen, one investor who sold their Bored Ape at the top of the market made a return of 41,326 per cent: the equivalent of cashing in a Bitcoin purchased in October 2013. But while these numbers were catnip to speculators, the reality for most was very different.

In a study of NFT marketplaces across 2021, Chainalysis found that only 22 per cent of ‘unwhitelisted’ buyers (ie those who bought their tokens via public exchanges rather than advanced pre-sales) made a profit, while 59 per cent lost at least half their original stake.

Content from our partners

[See also: What you need to know before investing in NFTs]

What’s more, profitable trades were highly concentrated. Indeed, the report found that just 5 per cent of users made 80 per cent of profitable trades. One plausible explanation is that, with the technology in its relative infancy, the market favoured established collectors; a small clique of experts who were able to monetise their knowledge.

Lawsuits and scams

Or could the truth be something more cynical entirely? Last December, two frustrated buyers of devalued NFTs filed a suit in California against the creator of Bored Apes (Yuga Labs), accusing the company of conspiring with celebrities – and crucially the A-list talent agent Guy Oseary – to artificially inflate the price of certain Apes above others. Oseary and Yuga deny the allegations, with a decision on whether the case will proceed to trial expected this year.

Whatever the truth about Bored Apes, there’s no question that some buyers of other NFTs were cheated. In March 2022, US prosecutors charged two 20-year-olds with wire fraud after they allegedly raised $1.1 million from retail investors for a collection of supposedly must-have NFTs that never materialised – a scam that will sound familiar to anyone who has paid attention to goings-on in the Wild West of unregulated cryptocurrency.

Hackers also found ways to get their hands on genuine NFTs – typically through the use of corrupted smart contracts which, under the guise of a legitimate transaction, would seize control of a user’s wallet. The Family Guy actor Seth Green became the target of such a scam and ended up paying almost $300,000 to recover his stolen tokens.

Not all NFTs are created equally

Some people have managed to find value in NFTs, even the ones that are least in demand. In 2022, three NFT enthusiasts in the US founded Unsellable, a company that exists to buy up unwanted NFTs (for the princely sum of $0.01), thus enabling the previous owners to write off the losses against their taxes. Unsellable then re-advertises the NFTs for sale on OpenSea (the company says its living collection will be ‘the ultimate artefact of a period in economic history’).

All these issues compounded to take the shine off these digital assets. Yet those who follow the world of crypto wealth closely say not all NFTs have suffered the same fate. ‘When you look at status tokens like Bored Apes, they’re still hugely attractive for collectors,’ says James Brockhurst, a private client lawyer at Forsters and the author of a practitioner’s guide to crypto-assets.

Indeed, at the time of writing, Bored Apes are still selling for around $80,000 – even if their celebrity super-fans aren’t so prominent. As in their heyday, some Apes fetch considerably more than others. On 25 April Taiwanese musician turned blockchain mogul Jeff Huang offloaded one of his collection – Ape #7403 – for almost $400,000.

And what of Beeple, whose Everydays once fetched $69 million? The market for his work today is ‘soft’, according to Philip Hoffman, chief executive of the Fine Art Group. If the NFT for the piece were sold today, he doubts the price would reach the same level – ‘or even close’. But, Hoffman qualifies, Beeple retains ‘a niche following of wealthy collectors. I will not be surprised if, in years to come, it might be worth more’.

The collectors spending big on fringe assets

So who are the collectors still spending large sums on fringe assets such as lesser-known Beeple works or Bored Apes? ‘There certainly aren’t many cases of trust companies being asked to hold NFTs,’ says Brockhurst. He points to unresolved issues around anti-money-laundering (particularly the fact that NFTs can be sold back and forth between anonymous wallets, in order to launder money or inflate prices) as a sticking point for private client lawyers.

For that reason, he says, reputable firms in the private client arena have often been reluctant to provide services related to NFTs. However, many do deal with the so-called ‘blue-chip’ cryptos – in particular Bitcoin and Ethereum. ‘Those assets have become much more mainstream among private banks and trust companies,’ says Brockhurst. ‘You have established policies in place in terms of how you hold them.’

[See also: How the rise of NFTs is changing the world of digital investing]

The gap between crypto and traditional financial

But there is still a disconnect. Brockhurst suggests that since the origin of much of the wealth now held in NFTs has its roots in the cryptosphere, it has remained siloed from the mainstream wealth management ecosystem. ‘One characteristic of crypto entrepreneurs is that they have an instinctive distrust of financial institutions,’ he says. ‘And that can extend to lawyers too’.

It’s certainly true that many crypto investors prefer to keep as much of their identity as private as possible. Prior to the big Beeple sale, little was known about the offline identity of MetaKovan, the pseudonymous buyer who had spent a sum equivalent to the cost of a private jet for a piece of digital art. After the Christie’s sale, the buyer emerged: Vignesh Sundaresan, a 32-year-old Indian national living in Singapore.

It took until November 2021 for a Reuters investigation to reveal that the self-styled angel investor had been one of the first backers of Ethereum, a highly successful cryptocurrency seen as the younger sibling to Bitcoin. He used the proceeds from this to back other ICOs (initial coin offerings). At the time of the auction, he had amassed more than $1 billion.

[See also: Why crypto assets are more taxing than you think]

Token rich, cash poor

Kingsley Napley partner James Ward, who heads the firm’s private client team, says investors may encounter problems when it comes to getting their wealth out of crypto or the metaverse. ‘We’ve advised a lot of clients looking to sell their crypto to buy things like property,’ he tells Spear’s. ‘That means having to prove your source of funds. And if you can’t do that, then you can’t use that money’.

Given that many crypto moguls have the vast bulk of their wealth in purely digital assets, that could prove a major impediment.

And what about those other great use cases for NFTs touted by the blockchain advocates in the frenzied days of 2021? ‘I think the best way to look at NFTs as a technology is that they’re still very much a solution in search of a problem,’ says David Abner.

‘We still haven’t seen anything that comes close to bridging that gap between blockchain enthusiasts and the real world’.

[See also: Financial crime: why the wealthy should worry about sanctions]

After a rush of high-end fashion brands launching their own tokens during the boom market – often with some success – there was a brief buzz that NFTs could be used as a certificate of ownership and authenticity for luxury goods.

According to blockchain analyst Dune, sales of NFTs released by luxury brands reached $245 million in 2022, with Dolce & Gabbana alone accounting for almost 10 per cent of that. In most cases, though, these fashion NFTs have functioned exactly like their cartoon peers: as prestige trading cards for online clout. And despite the initial excitement, take-up remains patchy.

In the meantime, perhaps the most important role NFTs have to play is as a diversifier or passion investment for the portfolios of people who made money from past surges in the value of cryptocurrency. Even if some of the hype and excitement has faded, that wealth hasn’t completely disappeared – at least not yet.