Recently, the government issued a consultation document on new legislation to extend HM Revenue & Customs’ powers of retribution for undeclared income and gains hidden offshore. It believes that offshore tax evasion is difficult to detect and therefore punishment should be severe in order to act as a deterrent. The consultation paper proposes to criminalise a failure to declare income and gains in an offshore bank account.

Furthermore, it is proposed that the crime should be considered a ‘strict offence’. This means that the intention of the taxpayer is not relevant to whether or not the crime has been committed. HMRC will not have to prove that the taxpayer intended to evade tax, although the judge may consider conduct and intent when sentencing.

The consequences of being found guilty seem draconian and disproportionate. The culprit could face a fine of 200 per cent of the undeclared tax and/or be sentenced to six months’ imprisonment, as well as losing anonymity and gaining a criminal record.

If this law is enacted, consultation is being sought on whether or not there should be a statutory defence. This means that a crime would not have been committed if the taxpayer can demonstrate that all reasonable precautions were taken, for example, by consulting a tax adviser.

Related

It is important to consider these proposals in relation to HMRC’s current powers. At present, most penalties are civil, not criminal. There are civil penalties for careless or deliberate errors or inaccuracies in any statement, declaration or by any other method, eg a taxpayer failing to declare an offshore bank account on his tax return. Such errors are not uncommon because historically many people were encouraged by their bank manger to open an offshore account and have confused interest paid tax-free with interest free from tax.

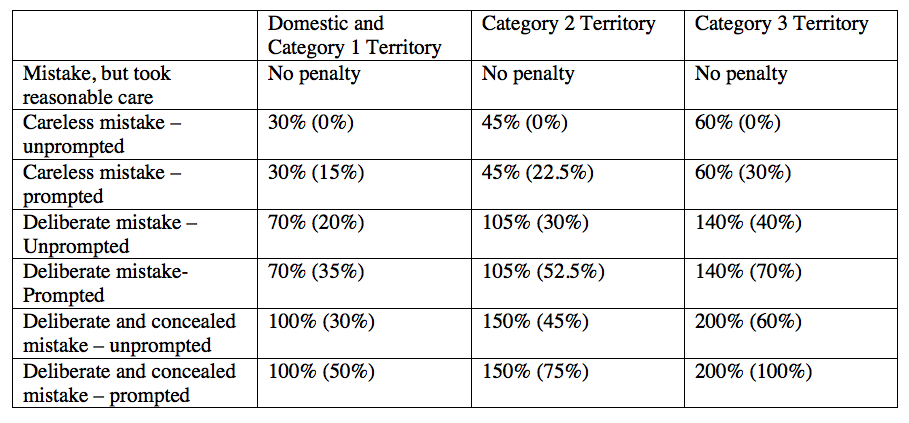

Under the current regime, penalties increase according to the severity of the failure. For example, an innocent mistake is unpunished providing the taxpayer took reasonable care in reporting; whereas a careless mistake is punishable by a penalty of between 30 and 60 per cent. The new proposal of ‘strict offence’ would mark a grave departure to prosecute those who perpetrate evasion by mistake.

When imposing penalties other factors are taken into account, such as whether the taxpayer voluntarily discloses the matter (unprompted) or at HMRC’s instigation (prompted) and in what jurisdiction the income or gains were hidden. Monies hidden in a UK or Category 1 territory, such as Guernsey, are jurisdictions where the HMRC can readily obtain information. However, at the other end of the spectrum, Category 3 territories, such as the Seychelles and the Cook Islands, are more opaque in their disclosure of information

The penalty is a percentage of the tax due. This table shows the maximum penalty which can be levied with the minimum penalty given in brackets. This gives the inspector some leeway to reward cooperation and the volunteering of information.

Content from our partners

In addition to the civil penalty regime HMRC also has access to criminal laws with more severe punishments where there is an element of deception or fraud.

The Taxes Management Act 1970 defines the crime of fraudulent evasion of income tax. This is where a person is knowingly concerned in the fraudulent, ie dishonest, evasion of income tax. The penalty for being found summarily guilty is up to twelve months in jail and or a fine of £5,000 and for indictable offences the penalty is up to seven years in jail and or an unlimited fine.

The Fraud Act 2006 applies where a taxpayer makes false representations to HMRC which are untrue or misleading and he knows that the representations are or could be untrue. False representations can include the failure to make a return, ie an act of omission rather than a positive act of deception. It is also a crime to obtain a tax advantage by deception or false accounting and to dishonestly fail to disclose information to HMRC when under a legal duty to do so.

The Theft Act 1968 provides that it is a crime to behave fraudulently resulting in a loss of revenue to HMRC to which it is entitled.

Finally, the Perjury Act 1911 can be applied where a taxpayer knowingly and wilfully makes materially false statements or returns for tax purposes.

The public might be forgiven for thinking that a new law is needed because HMRC lacks the necessary powers to do their job. However, this is not the case as HMRC already has a panoply of legislation which can be lawfully applied to delinquent taxpayers.

In my view, HMRC’s time would be better spent working within, or amending, the existing framework instead of introducing more penalties which will punish inadvertent evasion as harshly as wilful acts of deception.

Mark Davies is managing director of Mark Davies & Associates